A Consignment Account is a Nominal Account. It is classified as a nominal A/c because it is prepared to ascertain the profit earned or loss incurred on the consignment. The accounting rule applied to consignment A/c: Debit all Expenses & Losses and Credit all Incomes & Gains. As per the modeRead more

A Consignment Account is a Nominal Account. It is classified as a nominal A/c because it is prepared to ascertain the profit earned or loss incurred on the consignment.

The accounting rule applied to consignment A/c: Debit all Expenses & Losses and Credit all Incomes & Gains.

As per the modern rules, there is no clear-cut classification of consignment A/c. It is prepared from the perspective of the consignor, hence it cannot be outrightly classified as an expense/revenue.

In the context of accounting, consignment refers to an arrangement of goods wherein the consignor sends the goods to the consignee so that the consignee can sell/distribute the goods on behalf of the consignor.

The relationship between the consignor and consignee is that of a principal and agent. The consignee gets a commission for his services.

You should keep in mind that the consignee does not get ownership of the goods even though the goods are in his possession. The ownership remains with the consignor till the sale is made. On sale, the buyer will become the owner.

A Consignment A/c is an account prepared to record the transactions happening in a consignment business. This account is maintained by the consignor. It shows the profit earned or loss incurred by the consignor on a specific consignment.

A consignor may send goods to more than one consignee. In such a case, a separate consignment A/c is prepared for each consignment.

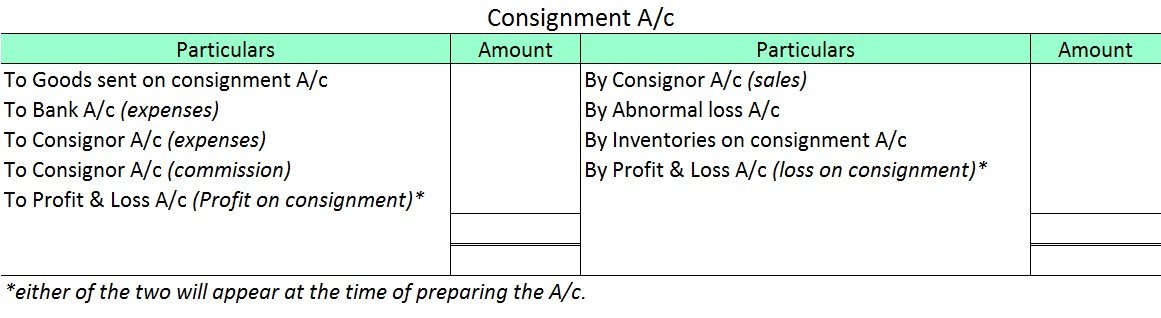

The following items appear on the debit side of the consignment A/c:

- Cost of goods sent on consignment.

- Expenses incurred by the consignor (freight, insurance, etc.)

- Expenses paid by the consignee (storage and warehousing, marketing expenses, packaging and selling expenses, etc.)

- Bad debts in consignment.

- Commission paid to consignee.

The entries appearing on the credit side of the consignment A/c are as follows:

- Gross sales.

- Abnormal loss of goods.

- Inventories on consignment (stock in transit).

The balance in the consignment A/c represents the profit or loss made on the consignment. It is transferred to the P&L A/c and the account is closed.

Below is the format for Consignment A/c:

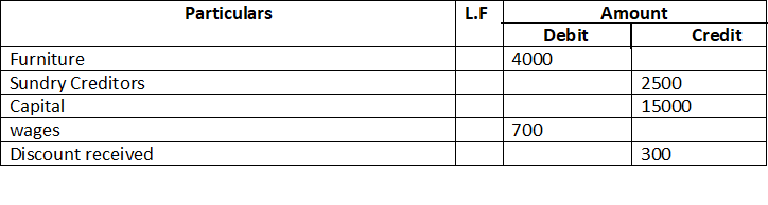

The trial balance shows the opening balance of various accounts. Now posting them in ledger accounts.

The trial balance shows the opening balance of various accounts. Now posting them in ledger accounts.

A statutory reserve is any reserve that has to be maintained by an Act or law. When it comes to insurance, a statutory reserve is a reserve that an insurance company is legally bound to maintain to ensure that the company is able to meet its policy obligations. In India, as per the Banking RegulatioRead more

A statutory reserve is any reserve that has to be maintained by an Act or law. When it comes to insurance, a statutory reserve is a reserve that an insurance company is legally bound to maintain to ensure that the company is able to meet its policy obligations. In India, as per the Banking Regulations Act, every banking company has to maintain at least 25% of its net profits as statutory reserves.

The companies are required to maintain such reserves to guarantee the availability of cash when it is required by the customer. Common examples of statutory reserves are Cash reserve ratio (CSR), Statutory Liquidity Ratio (SLR).

Treatment

Method

Rule-Based Approach – The company calculates the amount required by using standard formulas. However, since they are pre-determined formulas, it does not cover all risk determining factors.

Principle-based approach – This method is used to protect customers and ensure that the company stays solvent. They hold a higher amount of reserves than required after predicting all possible risks.

Statutory reserves are different from general reserves as general reserves are maintained voluntarily by the company. A company that does not follow statutory requirements will face financial penalties. These reserves are mostly maintained in the form of cash.

Maintenance of reserves gives confidence to investors that their money is secure. However, funds from these reserves can be used only for specific purposes. They should also maintain such reserves whether or not they earn profits.

See less