Definition Contingent Asset is an asset the existence, ownership, or value of which may be known or determined only on the occurrence or non-occurrence of one or more uncertain future events. However, the difference between Contingent assets is not disclosed whereas Contingent liabilities are discloRead more

Definition

Contingent Asset is an asset the existence, ownership, or value of which may be known or determined only on the occurrence or non-occurrence of one or more uncertain future events.

However, the difference between Contingent assets is not disclosed whereas Contingent liabilities are disclosed by way of notes they do have different criteria for recognition which are discussed below.

For example:– a claim that an enterprise is pursuing through the legal process, where the outcome is uncertain, is a contingent asset.

Contingent liabilities are defined as obligations relating to existing conditions or situations which may arise in the future depending on the occurrence or non-occurrence of one or more uncertain events.

For example:- Billis discounted but not yet matured, arrears of dividend on cum –preferences-shares, etc.

Meaning as per AS – 29

Now let me try to explain to you the meaning according to Accounting Standard 29 of the above contingent assets and liabilities which is as follows:-

• Contingent asset

A contingent asset is a possible asset that arises from past events the existence of which will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events.

Not wholly within the control of the enterprise.

It usually arises from unplanned or unexpected events that give rise to the possibility of an inflow of economic benefits to the enterprise.

• Contingent liability

A possible obligation that arises from past events the existence of which will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events.

Not wholly within the control of the enterprise.

A present obligation that arises from past events but is not recognized because it is not probable that the outflow of resources embodying economic benefits will be required to settle the obligation or,

A reliable estimate of the amount of obligation cannot be made.

Recognition In Financial Statements

Contingent assets and liabilities are recognized as follows:-

• Contingent Assets

As per the prudence concept s well as present accounting standards, an enterprise should not recognize a contingent asset.

It is possible that the recognition of contingent assets may result in the recognition of income that may never be realized.

However, when the realization of income is virtually certain, the related asset no longer remains contingent.

• Contingent liability

As per the rules, it is not recognized by an enterprise.

When recognized?

Contingent assets are assessed continually and if it has become virtuality an outflow of economic benefits will arise.

The assets and the related income are recognized in the financial statements of the period in which the change occurs.

Contingent liability is assessed continually to determine whether an outflow of resources embodying economic benefits has become probable.

And if it becomes probable that an outflow or future economic benefits will require for an item previously dealt with as a contingent liability.

A provision is recognized in financial statements of the period in which the change probability occurs except in extremely rare circumstances where no reliable estimate can be made.

Disclosure

Now we will see how contingent assets and liability are disclosed which is mentioned below:-

• Contingent asset

These contingent assets are not disclosed in financial statements.

A contingent asset is usually disclosed in the report of the approving authority ( ie.e., Board Of Directors in the case of a company, and the corresponding approving authority in case of any enterprise), if ab inflow of economic benefits is probable.

• Contingent Assets

A contingent liability is required to be disclosed by way of a note to the balance sheet unless the possibility of an outflow of a resource embodying economic benefit is remote.

See less

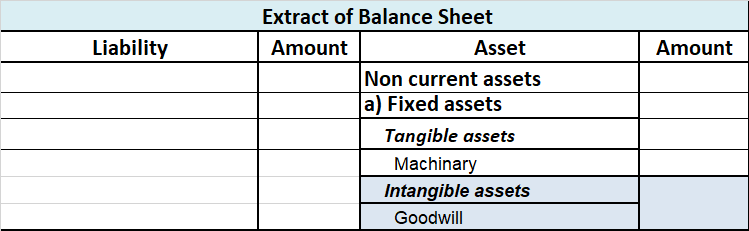

Goodwill In Accounting Aspect, Goodwill refers to an Intangible asset that facilitates a company in making higher profits and is a result of a business’s consistent efforts over the past years which can be the business's prestige, reputation, good name, customer trust, quality service, etc. GoodwillRead more

Goodwill

In Accounting Aspect, Goodwill refers to an Intangible asset that facilitates a company in making higher profits and is a result of a business’s consistent efforts over the past years which can be the business’s prestige, reputation, good name, customer trust, quality service, etc.

Goodwill has no separate existence although the concept of goodwill comes when a company acquires another company with a willingness to pay a higher price over the fair market value of the company’s net asset in simple words the goodwill can be only realized while at the time of sale of a business.

The formula for Goodwill

Types of Goodwill

there are two types of goodwill.

1. Inherent Goodwill/Self-generated goodwill

Inherent goodwill is the internally generated goodwill that was created or generated by the business itself. it is generally generated from the good reputation of the business.

Inherent Goodwill or Self-generated goodwill is generally not shown in the books or never recognized in the books of Accounts and no journal entry for the inherent goodwill is passed.

2. Purchased Goodwill/Acquired Goodwill

At the time of acquisition of a business by another business, any amount paid over and above the net assets simply refers to the amount of Purchased Goodwill or Acquired goodwill.

A Journal entry is passed in the case of the Purchase of goodwill.

Type of Account

generally, Goodwill is considered and recorded as an Intangible asset(long-term asset) due to its physical absence like other long-term assets.

Modern rule of accounting:

as per the Modern rule of accounting, all Assets or all possessions of a business are comes under the head Asset accounts.

as Goodwill is treated as an Intangible asset it is an Asset Account.

Journal entry for purchase of goodwill as per Modern rule

Goodwill A/c Dr. – Amt

To Cash/Bank A/c – Amt

(The modern approach of accounting for the Asset account is: “Debit the increase in asset and Credit the decrease in the asset“)

The golden rule of accounting

As per the golden rule of accounting, all assets or possessions of a business other than those which are related to any person (debtor’s account) are considered Real accounts.

Such accounts don’t close by the year-end and are carried forward.

As Goodwill is an Intangible asset it is treated as a Real account as per the golden rule of accounting.

Journal entry for purchase of goodwill as per Golden rule

Goodwill A/c Dr. – Amt

To Cash/Bank A/c – Amt

(The golden rule of accounting for the Real account is: “Debit what comes in and Credit what Goes out“)

See less