Net credit sales can be defined as the total sales made by a business on credit over a given period of time less the sales returns and allowances and discounts such as trade discounts. Net Credit Sales = Gross Credit Sales – Returns – Discounts – Allowances. Credit sales can be calculated from the ARead more

Net credit sales can be defined as the total sales made by a business on credit over a given period of time less the sales returns and allowances and discounts such as trade discounts.

Net Credit Sales = Gross Credit Sales – Returns – Discounts – Allowances.

Credit sales can be calculated from the Accounts receivable/ Bills Receivable/ Debtors figure in the Balance Sheet. It will be normally shown under the Current Assets head in the Balance Sheet.

Credit sales = Closing debtors + Receipts – Opening debtors.

Alternatively, you may observe the bills receivable ledger account to locate the figure of credit sales.

Net Credit Sales and related terms

Before we try to understand the concept of net credit sales with an example, let us discuss the term sales return. Sales return means the goods returned by the customer to the seller. It may be due to defects or any other reasons.

Now let us take an example. John is a retail businessman. He sells smartphones. He buys 100 smartphones from Vivo on credit. The smartphones are worth ₹1.5 lahks. He then returns smartphones worth 20,000 rupees to Vivo. He also gets an allowance of rupees 5,000 from Vivo.

In the above example, the credit sales of Vivo are of rupees 1.5 lakh. The net credit sales is of

1.5 lakh – 20,000 – 5, 000 = 1.25 lakh rupees.

Importance of Net Credit Sales

- Net Credit Sales figure together with the accounts receivable figure acts as an indicator of the credit policy of the company.

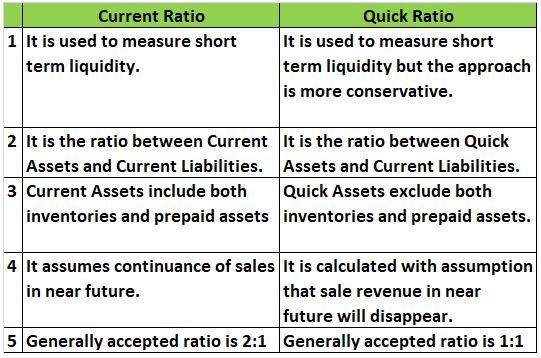

- It offers insights into the ability of the company to meet short-term cash obligations.

- The credit policy also affects the total current assets that the company has in the manifestation of Accounts Receivable

Advantages and Disadvantages of Credit Sales.

Advantages

- Increased Sales – The credit Policy facilitates increased sales for the company. The company can attract more customers with a liberal credit policy. For example, Apple got more customers when it started to sell its products on an EMI basis.

- Customer Loyalty / Retention- Regular customers can be retained and made to feel honored by offering them more liberal credit terms.

Disadvantages

- Delay in Cash Collection – Credit Sales imply that the company would get cash on a delayed basis. This money could have otherwise been put to use for some other profitable venture or could have borne interest for the company

- Collection Expenses– The company had to incur additional expenditures for collecting money from debtors.

- Risk of Bad Debts – With credit sales, there is always the risk that the buyer may become bankrupt and may not be able to pay the money due to the seller.

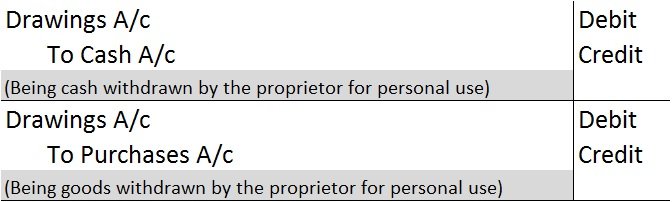

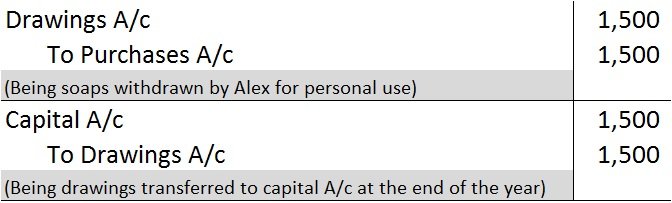

When a company issues shares to shareholders at a price over the face value (at a premium), that amount is termed as securities premium. This amount is transferred to what we call the securities premium reserve. The company is required to maintain a separate reserve for securities premium. UtilizatiRead more

When a company issues shares to shareholders at a price over the face value (at a premium), that amount is termed as securities premium. This amount is transferred to what we call the securities premium reserve. The company is required to maintain a separate reserve for securities premium.

Utilization

Securities premium reserve can be used for the following reasons:

Since it is not a free reserve, it can only be used for a few specific purposes. The amount received as securities premium cannot be used to transfer dividends to shareholders

Treatment

When a company issues shares at a premium, the securities premium reserve account is credited along with share capital as an increase in capital is credited according to the modern rule of accounting.

For example,

Sonly Ltd. issues 1,000 shares of $10 face value at $15. Here, the amount of premium would be $5 (15 – 10) per share. Therefore, the journal entry would show:

Bank a/c (15 x 1,000) Dr 15,000

To Share Capital (10 x 10,000) 10,000

To Securities Premium Reserve a/c (5 x 10,000) 5,000

From the above example, we can see that the company receives $15,000, but transfers $10,000 to share capital and the excess $5,000 to securities premium reserve.

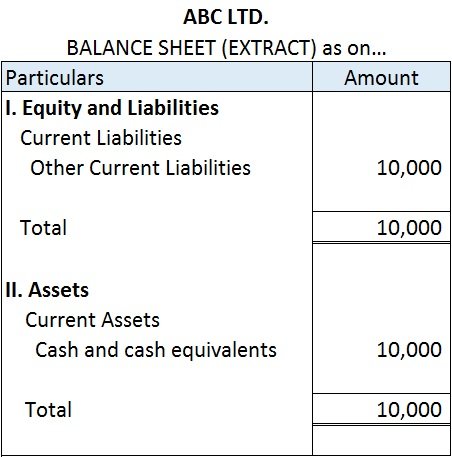

In the balance sheet, this securities premium reserve is shown under the title “Equity and Liabilities” under the head ‘‘Reserves and Surplus”.

See less