What is Impairment of Assets? Impairment of assets means a decline in the value of assets due to unforeseen circumstances. Assets are impaired when the carrying value of assets increases its market value or “realizable value”. Impairment can be caused due to factors that are internal or external toRead more

What is Impairment of Assets?

Impairment of assets means a decline in the value of assets due to unforeseen circumstances. Assets are impaired when the carrying value of assets increases its market value or “realizable value”.

Impairment can be caused due to factors that are internal or external to the firm. Internal factors such as physical damage, obsolescence or poor management and external factors such as a change in legal or economic circumstances, increased competition or reduction in asset’s fair value in the market result in impairment.

Impairment Vs Depreciation

Asset impairment is often confused with asset depreciation, which is rather a recurring and expected event, unlike impairment that reflects an abrupt decrease in the value of the asset.

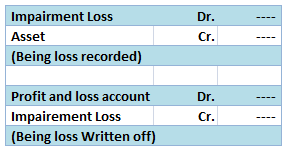

Impairment Loss

Impairment is always treated as a loss in accounting. It is the amount by which the carrying value or the asset’s book value exceeds its fair market value.

Before recording Impairment loss, a company must determine the recoverable value of the asset which is higher of the asset’s net realizable value or value in use. Then it is to be compared with the book value of the asset.

If the carrying value exceeds the recoverable value then the impairment loss is to be recorded at the exceeding value i.e. difference of carrying value and realizable value.

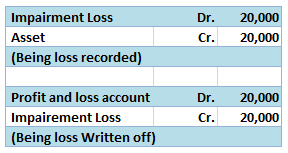

Example

Suppose a company Royal Ltd. has an asset with a carrying value of 50,000, which has suffered physical damage. According to the company’s calculation, the asset has a net realizable value of 30,000 and a value in use of 25,000.

Then, the recoverable value would be higher of the asset’s net realizable value or value in use, i.e., 30,000 which is still lower than the carrying amount of 50,000. Therefore, Royal ltd. will have to record 20,000 (50,000-30,000) as impairment loss.

This is will increase Royal Ltd’s expenses by 20,000 and decrease the asset’s value by the same amount.

See less

Definition Debit balance may arise due to timing differences in which case income will be accrued at the year's end to offset the debit. The amount is shown in the record of a company s finances, by which its total debits are greater than its total credits. The account which has debit balances are aRead more

Definition

Debit balance may arise due to timing differences in which case income will be accrued at the year’s end to offset the debit.

The amount is shown in the record of a company s finances, by which its total debits are greater than its total credits.

The account which has debit balances are as follows:

• Assets accounts

Land, furniture, building machinery, etc

• Expenses accounts

Salary, rent, insurance, etc

• Losses

Bad debts, loss by fire, etc

• Drawings

Personal drawings of cash or assets

• Cash and bank balances

Balances of these accounts

In class 11th, we learned about all these accounts that have debit balances.

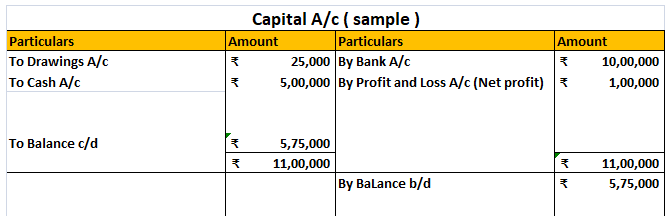

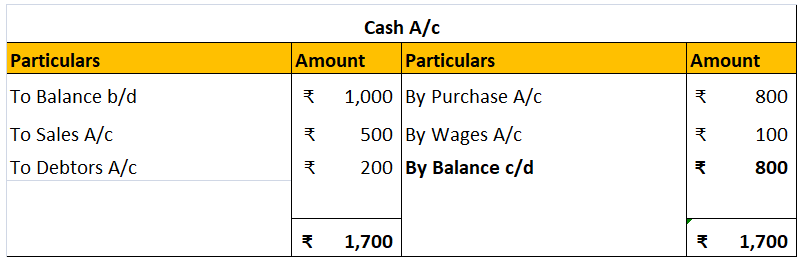

Where the total of the debit side is more than the credit side therefore the difference is the debit balance and is placed credit side as “ by balance c/d “

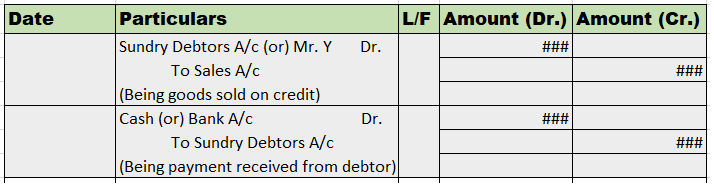

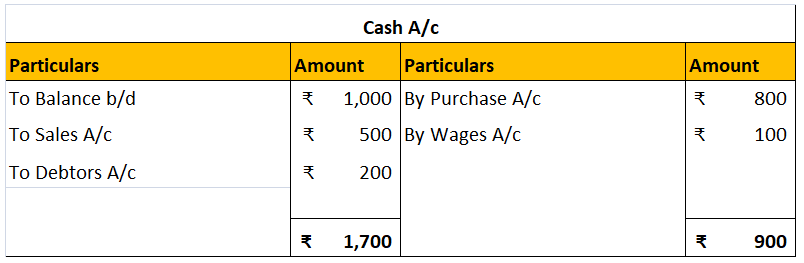

Here are some examples showing the debit balances of the accounts :

See less