When a partnership firm consisting of some partners, decide to admit a new partner into their firm, they have to forego a part of their share for the new partner. Therefore, sacrificing Ratio is the proportion in which the existing partners of a company give up a part of their share to give to the nRead more

When a partnership firm consisting of some partners, decide to admit a new partner into their firm, they have to forego a part of their share for the new partner. Therefore, sacrificing Ratio is the proportion in which the existing partners of a company give up a part of their share to give to the new partner. The partners can choose to forego their shares equally or in an agreed proportion.

Before admission of the new partner, the existing partners would be sharing their profits in the old ratio. Upon admission, the profit-sharing ratio would change to accommodate the new partner. This would give rise to the new ratio. Hence Sacrificing ratio can be calculated as:

Sacrificing Ratio = Old Ratio – New Ratio

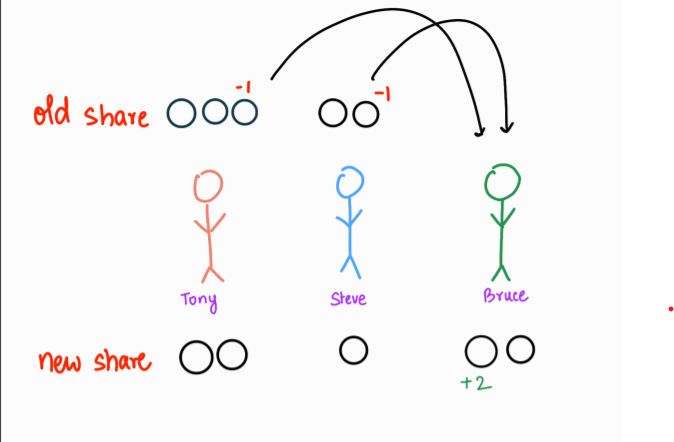

For example, Tony and Steve are partners in a firm, sharing profits in the ratio of 3:2. They decide to admit Bruce into the partnership such that the new profit-sharing ratio is 2:1:2. Now, to calculate the sacrificing ratio of Tony and Steve, we subtract their new share from their old share.

Tony’s Sacrifice = 3/5 – 2/5 = 1/5

Steve’s Sacrifice = 2/5 – 1/5 = 1/5

Therefore, the Sacrificing ratio of Tony and Steve is 1:1. This shows that Tony gave up 1/5th of his share while Steve also sacrificed 1/5th of his share.

Calculation of sacrificing ratio is important in a partnership as it helps in measuring that portion of the share of existing partners that have to be sacrificed. This ensures a smooth reconstitution of the partnership. Since the old partners are foregoing a part of their share in profits, the new partner has to bring in some amount as goodwill to compensate for their loss.

See less

Profits earned by a firm are not completely distributed to its owners, some of the profits are retained for various purposes. Reserves are profits that are apportioned or set aside to use in the future for a specific or general purpose. Reserves follow the Conservative Principle of accounting. ReveRead more

Profits earned by a firm are not completely distributed to its owners, some of the profits are retained for various purposes. Reserves are profits that are apportioned or set aside to use in the future for a specific or general purpose. Reserves follow the Conservative Principle of accounting.

Revenue reserve is created from the net profits of a company during a financial year. Revenue reserve is created from revenue profit that a company earns from the daily operations of the business.

Various types of reserves are:

Different parts of profit are apportioned to create a different reserve and those reserves can only be used for purposes as defined.

While accounting for Revenue Reserve, the profit decided to transfer to Revenue Reserve are first transferred to Profit and Loss Appropriation Account and then to Revenue Reserve Account. In the balance sheet, Revenue Account is shown under the Capital and Reserves head.

Uses of Revenue Reserve:

Example:

Given that Revenue Reserve Account stands at Rs 1,00,000 and the company wants to distribute Rs. 40,000 as dividend to its shareholders. The treatment of this transaction in the financial statements will be-

Particulars Amount (Rs.)

Revenue Reserve Account 1,00,000

(less) Dividend distributed (40,000)

The amount shown in Balance Sheet 60,000

See less