Definition Bad debts are a debt owed to an enterprise that is considered to be irrecoverable or we can say that it is owed to the business that is written off because it is irrecoverable. Sometimes debtors are unable to pay the amount due either partially or fully. the amount that is not receivableRead more

Definition

Bad debts are a debt owed to an enterprise that is considered to be irrecoverable or we can say that it is owed to the business that is written off because it is irrecoverable.

Sometimes debtors are unable to pay the amount due either partially or fully. the amount that is not receivable is a loss and is called bad debt.

Bad debts are neither assets nor liabilities they are expenses that are debited to the profit and loss account and reduced from debtors in the balance sheet.

For example loans from banks are declared as bad debt, sales made on credit and amounts not received from customers, etc.

Related terms

So there are a few related terms whose meanings you should know

- Further bad debts :

- It means the amount of sundry debtors in the trial balance is before the deduction of bad debts. in this situation, entry for further bad debts is also passed into the books of account.

- That is bad debts are debited and the debtor’s account is credited. And the accounting treatment for them is the same as bad debts which I have shown you above.

- Bad debts recovered :

- It may happen that the amount written off as bad debts are recovered fully or partially.

- In that case, the amount is not credited to the debtor’s (personal) account but is credited to the bad debts recovered account because the amount recovered had been earlier written off as a loss.

- Thus amount recovered is a ‘gain’ and is credited to the profit and loss account.

Accounting methods

There are two methods for accounting for bad debts which are mentioned below:-

- First, is the direct written-off method which states that bad debts will be directly treated as expenses and expensed to the income statement, which is called the profit and loss account.

- Second, is the allowance method which means we create provisions for doubtful debts accounts and the debtor’s account remains as it is since the debtor’s account and provision for doubtful debts account are two separate accounts.

-

- Debts that are doubtful of recovery are provided estimating the debts that may not be recovered .amount debited to the profit and loss account reduces the current year’s profit and the amount of provision is carried forward to the next year.

-

- Next year, when debts actually become bad debts and are written off, the amount of bad debts is transferred ( debited ) to the provision for doubtful debts account.

-

- The amount of bad debts is not debited to the profit and loss account since it was already debited in earlier years.

-

- Provision for doubtful debts is shown in the debit side of the profit and loss account as well as shown as a deduction from sundry debtors in the assets side of the balance sheet.

Accounting treatment

Now let me try to explain to you the accounting treatment for bad debts which is as follows :

- Balance sheet

-

- In the balance sheet either it can be shown on the asset side under the head, current assets by reducing from that specific assets.

-

- For example, if credit sales are made to a customer who says it’s not recoverable or is partially recoverable then the amount is bad debt. It’s a loss for the business and credited to the personal account of debtors or we can say reduced from debtor those are current assets of the balance sheet.

- Profit and loss account

-

- Bad debts are treated as expenses and debited to the profit and loss account.

- For example, as I have explained above, before transferring to the balance sheet, bad debt will be debited to the profit and loss account as an expense.

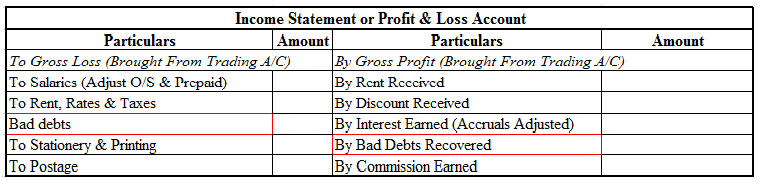

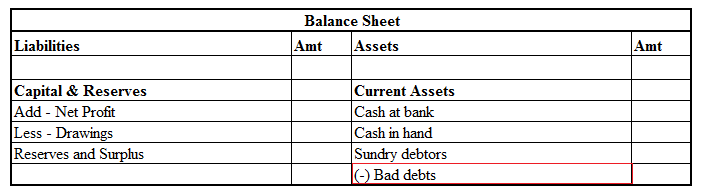

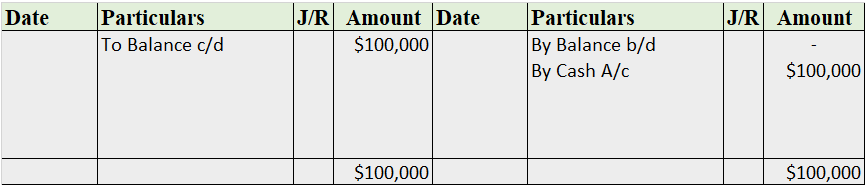

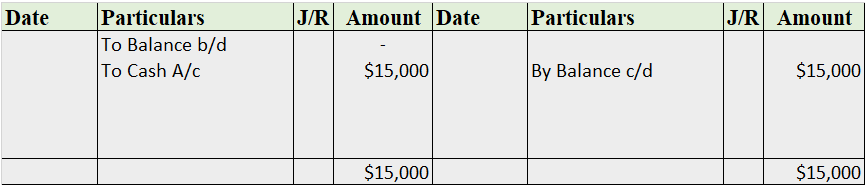

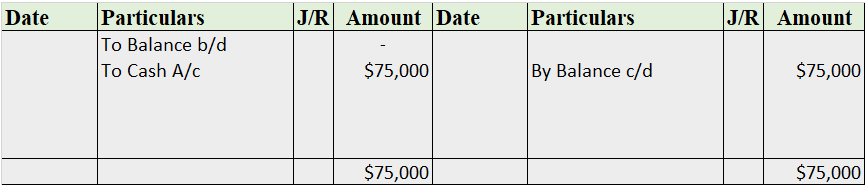

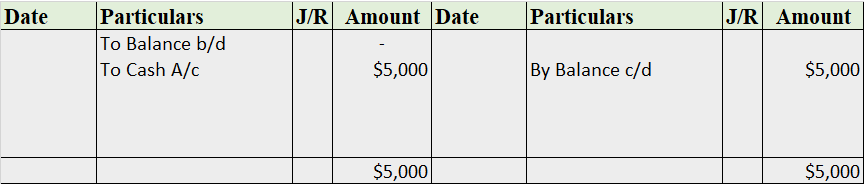

Now let me show you the extract of the profit and loss account and balance sheet showing bad debts and bad debts recovered which are as follows:-

Generally, Assets are classified into two types. Non-Current Assets Current Assets Non-Current Asset Noncurrent assets are also known as Fixed assets. These assets are an organization's long-term investments that are not easily converted to cash or are not expected to become cash within an acRead more

Generally, Assets are classified into two types.

Non-Current Asset

Noncurrent assets are also known as Fixed assets. These assets are an organization’s long-term investments that are not easily converted to cash or are not expected to become cash within an accounting year.

In general terms, In accounting, fixed assets are assets that cannot be converted into cash immediately. They are primarily tangible assets used in production having a useful life of more than one accounting period. Unlike current assets or liquid assets, fixed assets are for the purpose of deriving long-term benefits.

Unlike other assets, fixed assets are written off differently as they provide long-term income. They are also called “long-lived assets” or “Property Plant & Equipment”.

Examples of Fixed Assets

Valuation of Fixed asset

fixed assets are recorded at their net book value, which is the difference between the “historical cost of the asset” and “accumulated depreciation”.

“Net book value = Historical cost of the asset – Accumulated depreciation”

Example:

Hasley Co. purchases Furniture for their company at a price of 1,00,000. The Furniture has a constant depreciation of 10,000 per year. So, after 5 years, the net book value of the computer will be recorded as

1,00,000 – (5 x 10,000) = 50,000.

Therefore, the furniture value should be shown as 50,000 on the balance sheet.

Presentation in the Balance Sheet

Both current assets and non-current assets are shown on the asset side(Right side) of the balance sheet.

Difference between Current Asset and Non-Current Asset

Current assets are the resources held for a short period of time and are mainly used for trading purposes whereas Fixed assets are assets that last for a long time and are acquired for continuous use by an entity.

The purpose to spend on fixed assets is to generate income over the long term and the purpose of the current assets is to spend on fixed assets to generate income over the long term.

At the time of the sale of fixed assets, there is a capital gain or capital loss but at the time of the sale of current assets, there is an operating gain or operating loss.

The main difference between the fixed asset and current asset is, although both are shown in the balance sheet fixed assets are depreciated every year and it is valued by (the cost of the asset – depreciation) and current asset is valued as per their current market value or cost value, whichever is lower.

See less