Non-debt capital receipts As we're aware, there are two main sources of the government’s income — revenue receipts and capital receipts. Revenue receipts are all those receipts that neither create any liability nor cause any reduction in assets for the government, whereas, capital receipts are thoseRead more

Non-debt capital receipts

As we’re aware, there are two main sources of the government’s income — revenue receipts and capital receipts. Revenue receipts are all those receipts that neither create any liability nor cause any reduction in assets for the government, whereas, capital receipts are those money receipts of the government that either create a liability for a government or cause a reduction in assets.

Revenue receipts comprise both tax and non-tax revenues while capital receipts consist of capital receipts and non-debt capital receipts. Non-debt capital receipt is a part of capital receipt.

Definition

Non-debt capital receipts, also known as NDCR, are the taxes and duties levied by the government forming the biggest source of its income. Those receipts of the government lead to a decrease in assets, and not an increase in liabilities. It accounts for just 3% of the central government’s total receipts.

The union government usually lists non-debt capital receipts in two categories:

- Recovery of loans – Recovery of loans means the amount recovered when a loan defaults.

- Other receipts – Other receipts basically mean disinvestment proceeds from the sale of the government’s share in public-sector companies.

- Money accrued to the union government from the listing of central government companies and the issue of bonus shares.

For Example – Disinvestment and recovery of loans are non-debt creating capital receipts.

See less

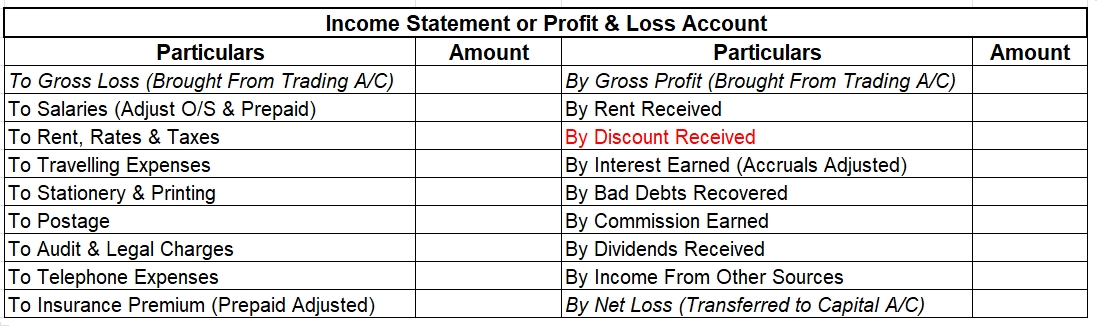

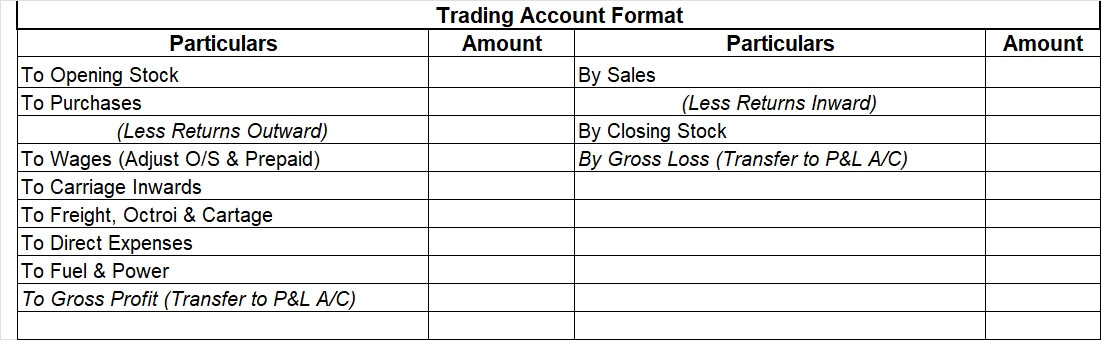

The profit and loss appropriation account is an account created in addition to the Trading & Profit and loss account in the case of partnership firms. It is a nominal account. The net profit or loss from the Profit and loss account is transferred to the Capital A/c when we do the accounting of sRead more

The profit and loss appropriation account is an account created in addition to the Trading & Profit and loss account in the case of partnership firms. It is a nominal account.

The net profit or loss from the Profit and loss account is transferred to the Capital A/c when we do the accounting of sole proprietors.

But, while doing the accounting of partnership, there is a need to appropriate this profit or loss as there are two or more partners’ capital accounts. So, for this purpose, the Profit and loss appropriation account is created.

The net profit or loss is appropriated among the partner’s capital after adjustment the items like partner’s salary, commission, interest on capital, interest on drawing etc. It consists of items related to the partner’s claim.

The format of the profit and loss appropriation account is as below:

Let solve a problem to sharpen our concept:

A and B are partners in firm sharing profits and losses in the ratio of 4:1. On 1st January 2019, their capitals were ₹ 20,000 and ₹ 10,000 respectively. The partnership deed specifies the following:

Prepare Profit and loss appropriation account for the year ending 31st December 2019.

Solution:

See less