Deferred Tax Liability A deferred tax liability represents an obligation to pay taxes in the future. These taxes are owed by a company but are not due to be paid until a future date. Companies that incur such an obligation prepare and maintain two financial reports every year: a tax statement and anRead more

Deferred Tax Liability

A deferred tax liability represents an obligation to pay taxes in the future. These taxes are owed by a company but are not due to be paid until a future date.

Companies that incur such an obligation prepare and maintain two financial reports every year: a tax statement and an income statement.

This is because companies maintain their books as per book accounting rules (GAAP/IFRS), but they have to pay taxes according to tax accounting rules, and they each have to follow their own guidelines.

For example, a tax statement follows the cash basis of accounting, and an income statement follows the accrual basis of accounting.

Companies calculate their profit as per the accounting rules as well as tax laws known as accounting income and taxable income, respectively. Some differences arise due to the application of different provisions of law.

These temporary differences are accounted for, recognized, and carried forward in the books of accounts and create deferred tax.

Example

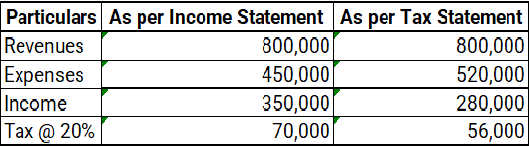

Here is an example of deferred tax liability.

In the given example, tax as per income statement is 70,000, whereas as per tax statement it is 56,000. This temporary difference is termed as deferred tax liability of 14,000.

When accounting income is more than taxable income, it creates Deferred Tax Liability. It will be adjusted in the books of accounts during one or more subsequent year(s).

How Does it Arise?

There are several instances under which a company creates a deferred tax liability. Some other instances are:

Depreciation Methods

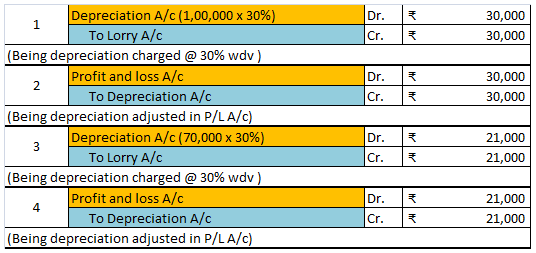

- One of the most common reasons for deferred tax liability is when a company uses different depreciation methods in the Income and Tax Statement.

- Assets are depreciated by calculating the straight-line method in the Income Statement, while the written-down value method is used in the Tax Statement.

- Since the straight-line value method produces lower depreciation when compared to the WDV method, accounting income is temporarily higher than taxable income.

- The company recognises deferred tax liability as this difference between accounting income and taxable income.

Treatment of Revenue & Expenses

- Deferred tax liability can also arise when there is a difference in the way revenue and expenses are treated in books of accounts.

- As mentioned earlier, accounting rules follow the accrual basis of accounting while tax laws follow the cash basis of accounting.

- Meaning in the tax statement, income and expenses are recorded when they are received or paid, not when they are incurred or realised.

- This difference in the treatment of revenue and expenses creates deferred tax liability.

Impact on Financial Statements

Recognising deferred tax liability and its subsequent effect on the company’s financial statement is important as it simplifies the process of auditing and analysing financial reports.

Balance Sheet

- Deferred tax liabilities are recorded on the liability side of the balance sheet under non-current liabilities.

Cash Flow Statement

- The deferred tax liability is added back to the net income in calculating cash flow from operating activities to show the actual cash flow.

Yes, the account receivable is a sub ledger account. It is an account that is used to record the payment history of each and every customer to whom the business has sold goods or provided services on credit. Accounts receivable represent the amount that the customers owe to the business with respectRead more

Yes, the account receivable is a sub ledger account. It is an account that is used to record the payment history of each and every customer to whom the business has sold goods or provided services on credit.

Accounts receivable represent the amount that the customers owe to the business with respect to the goods sold or services provided to them on credit. They are also known as trade receivable or debtors.

The accounts receivable subledger shows various details of every transaction like the invoice number, amount due, date of payment, discount allowed etc. The subledger accounts are also known as the subsidiary accounts.

Difference between general ledger and subledger accounts

Here is a list of the major differences between sub-ledgers and the general ledger:

Importance/ use of Subsidiary Account

The usefulness of an accounts receivable sub ledger account lies in the fact that it provides detailed information about the money different customers owe to the business.

For example, the general ledger account may show that the total balance of trade receivable is 1 lakh without indicating the individual amount that each customer owes to the business. The subsidiary account can help us by showing that customer A owes 50000 rupees, customer B owes 30000 rupees while customer C owes 20000 rupees.

In short, the subsidiary accounts provide detailed information about each and every transaction. They help us to find useful information quickly and easily. They help us analyze the business policies and take corrective actions.

Thus, we can conclude that accounts receivable is a subledger account that provides us detailed information about the various credit transactions and the amount that each customer owes to the business. It helps us analyze our credit policies and take corrective actions. It helps us identify and classify bad debts as such on

See less