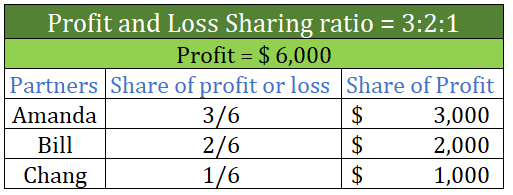

A revaluation Account is an account created to record the changes in the value of assets and liabilities during: Change in profit sharing ratio Admission of a partner Retirement of a partner Death of a partner The realization Account is prepared to sell assets and pay liabilities in the event of theRead more

A revaluation Account is an account created to record the changes in the value of assets and liabilities during:

- Change in profit sharing ratio

- Admission of a partner

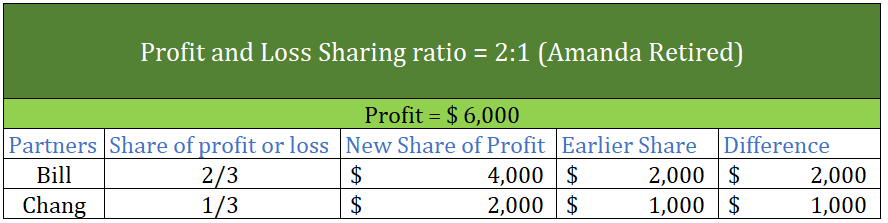

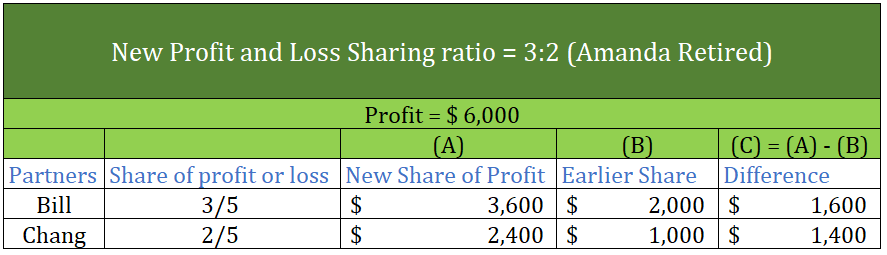

- Retirement of a partner

- Death of a partner

The realization Account is prepared to sell assets and pay liabilities in the event of the dissolution of the firm.

Revaluation Account is prepared for dissolution of the partnership while Realization Account is prepared for dissolution of the partnership firm.

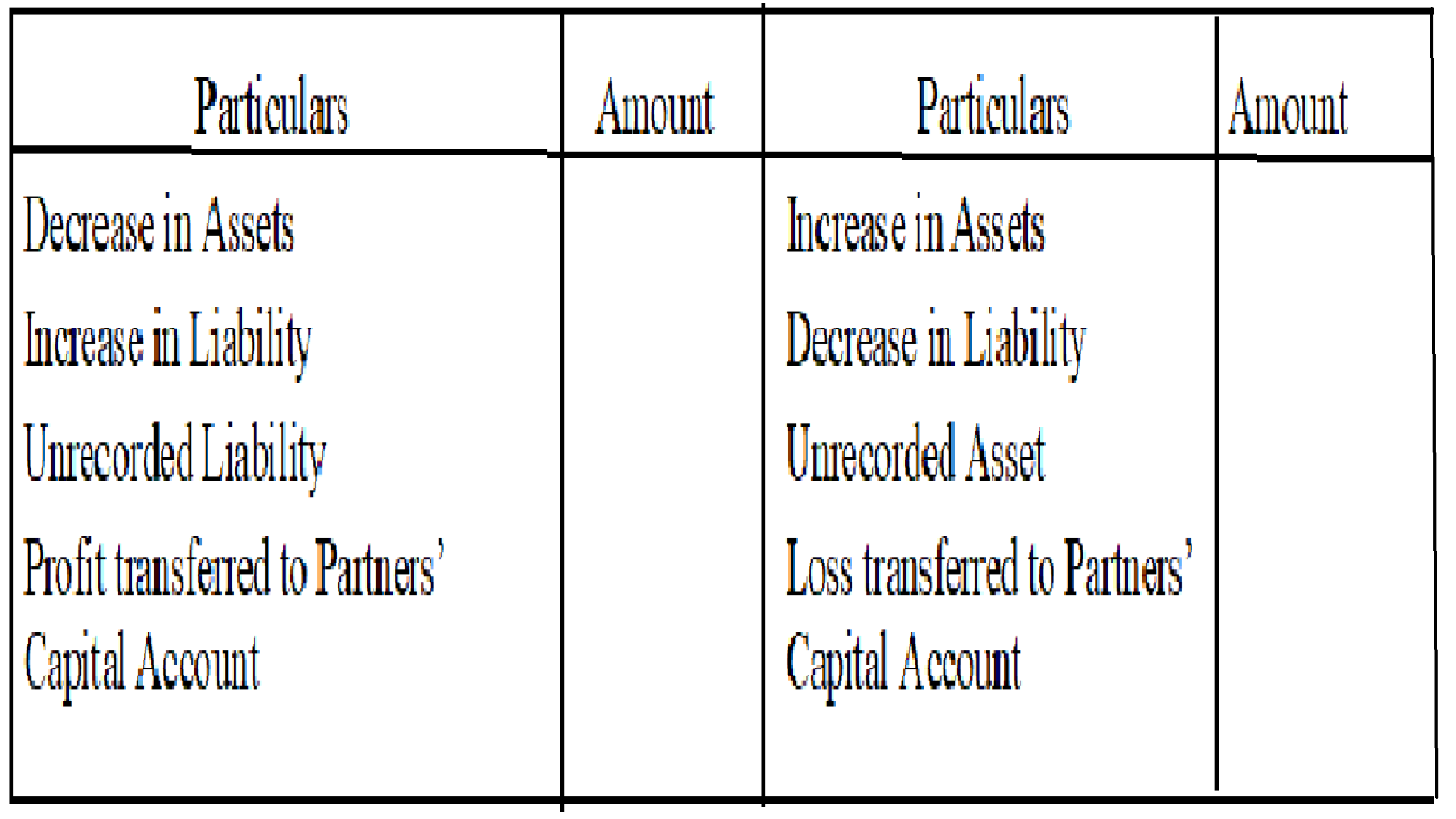

The increase or decrease in the value of assets and liabilities is transferred to the Realisation Account and the gain or loss thereof is transferred to the old partner’s capital account.

- A decrease in Assets and an Increase in Liabilities is debited since it is a loss for the firm and all the losses are debited.

- An increase in Assets and a Decrease in Liabilities is credited since it is gained for the firm and all the profits are credited.

Format of Revaluation Account will be:

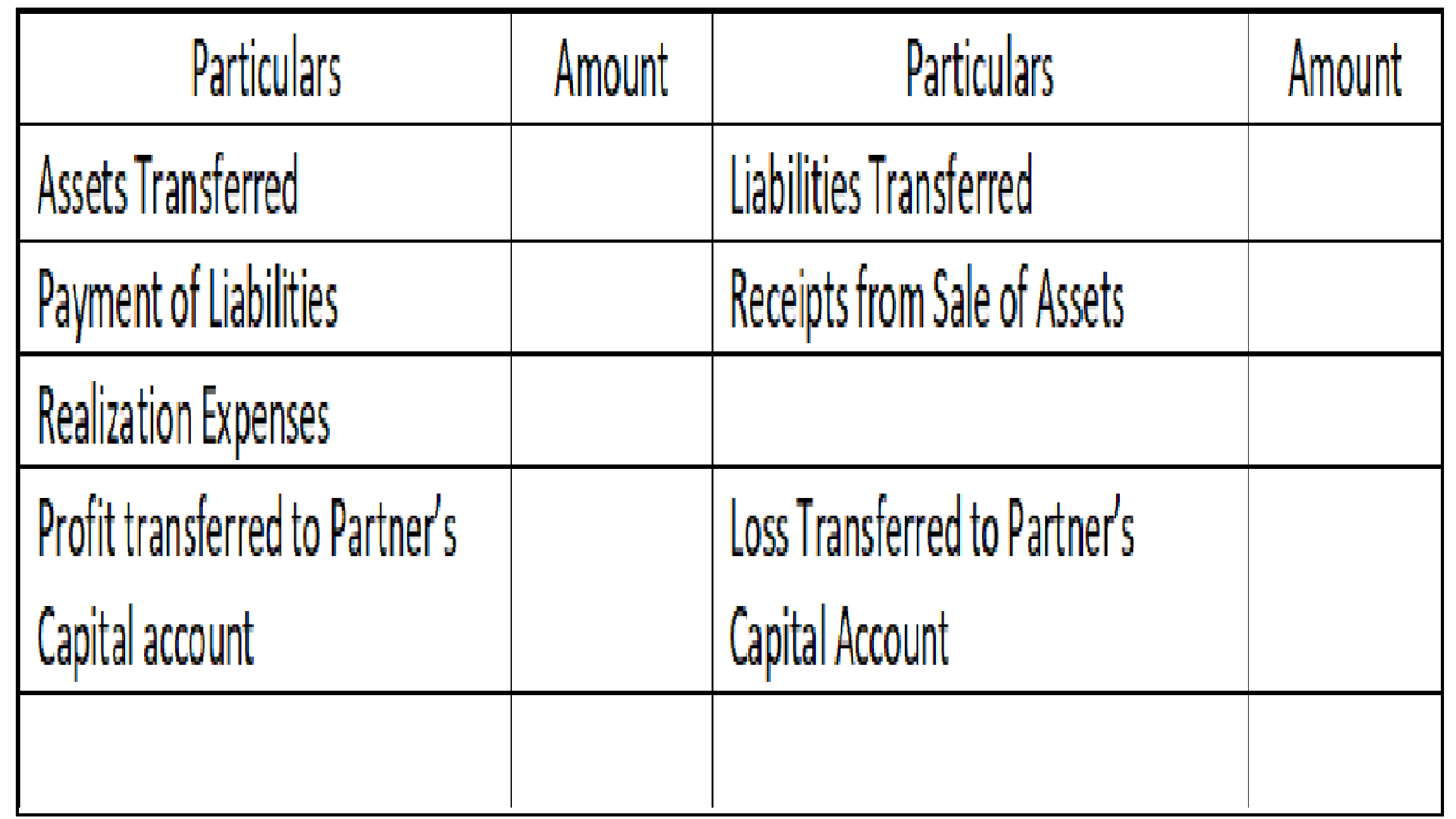

Format of Realization Account will be:

The difference between Realisation and Revaluation Account is:

| Revaluation Account | Realization Account |

| Prepared to record changes in assets and liabilities | Prepared to record sale of assets and payment of liabilities |

| Prepared at the time of dissolution of the partnership | Prepared at the time of dissolution of partnership firm |

| Assets and liabilities still exist in the books only their values change | Assets and liabilities do not exist in the books of the firm |

| This account contains only those assets and liabilities that are to be revalued. | This account contains all the assets and liabilities of the firm. |

| A revaluation Account can be prepared any number of times during the lifetime of the firm. | The realization Account is only made once during the dissolution of the firm. |

| The gain or loss during revaluation is transferred to the old partner’s capital accounts. | The gain or loss during realization is transferred to the capital account of all the partners. |

See less

Meaning of Workmen's Compensation Reserve Workmen compensation reserve is a reserve created to compensate the labourers and employees of a firm in case of an uncertain future event in the line with their work. For example, if a labourer or group of labourers get injured seriously while working on thRead more

Meaning of Workmen’s Compensation Reserve

Workmen compensation reserve is a reserve created to compensate the labourers and employees of a firm in case of an uncertain future event in the line with their work. For example, if a labourer or group of labourers get injured seriously while working on the premises of the firm, then they will be compensated from the money kept aside in the workmen’s compensation reserve.

Workmen’s compensation reserve is created using the profits of a business. The journal entry for the creation of workmen compensation reserve is as follows:

When a claim arises, the claim amount is transferred to Provision for workmen compensation claim A/c

Treatment of workmen compensation reserve in revaluation account

At the time of admission, retirement or death of partner or change in profit sharing ratio, the reserve is distributed among the old or existing partners or kept intact.

Workmen’s compensation reserve is also distributed among the old or existing partners subject to the claim arising on the reserve.

Here are the three situations:

The revaluation account comes into the picture only when the claim is more than the amount available in the reserve. For example, the claim is Rs. 20,000 but the amount in the reserve is only Rs. 15,000.

In such a case, the excess claim will be met by debiting the revaluation account.

The journal will as given below:

Since the revaluation account is debited, it is a loss and this loss will be written from old or existing partners’ capital in the old profit sharing ratio. The journal entry is given below:

See less