Introduction The term 'gain ratio' is related to partnership accounting. Gain ratio refers to the ratio in which existing partners of a partnership firm, divide among themselves, the share of profit and loss of the outgoing partners. There is a method of calculating this gain ratio. The method alongRead more

Introduction

The term ‘gain ratio’ is related to partnership accounting. Gain ratio refers to the ratio in which existing partners of a partnership firm, divide among themselves, the share of profit and loss of the outgoing partners.

There is a method of calculating this gain ratio. The method along with the concept behind gain ration is discussed below.

Concept behind gain ratio

A partnership firm is a form of business organisation which is conducted and carried on by members known as partners. It requires at least two partners to start a firm and the maximum limit is 50.

The partners share the profit and loss of a business in a ratio known as Profit and loss sharing ratio.

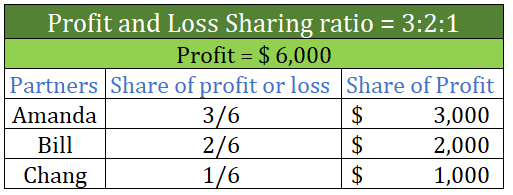

For example, Amanda, Bill and Chang are partners, having a P/L sharing ratio of 3:2:1 i.e. Amanda is getting 3/6, Bill is getting 2/6 of the same and Chang is getting ⅓ of the profit and loss

If the profit is $6,000 , then Amanda will get $3,000 (3/6 of $6,000) and Bill will get $2,000 (2/6 of $6,000) and Chang will get $1,000 (1/6 of $6,000).

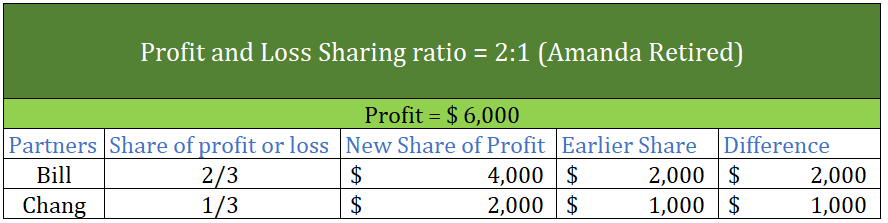

Now if Amanda retires from the firm, then naturally, Bill and Chang’s share of profit will increase.

The profit and loss sharing ratio will now be 2:1 (earlier it was 3:2:1) and the share of profit of Bill will be $4,000 and of Chang will be $2,000.

Calculation of gain ratio

The formula for calculating gain ratio = New ratio – Old Ratio

As per the above case:

- Gain ratio of Bill = 2/3 – 2/6 = 2/6

- Gain ratio of Chang = 1/3 – 1/6 = 1/6

Therefore the gain ratio in which Bill and Chang gained the share of profit of Amanda is 2/6 : 1/6 or simply 2:1

This is how we can calculate the gain ratio. But one thing to notice is that the gain ratio is equal to the P/L sharing ratio of the partnership between Bill and Chang.

Hence, whenever a partner retires and the existing partner keep the P/L sharing ratio unchanged among themselves then, the gain ratio will be equal to their P/L sharing ratio. In that case, there is no need to calculate the gain ratio from the formula given above.

But, when the remaining partners change the P/L sharing ratio among themselves after a partner retires, then the gain ratio is to be calculated using the formula given above.

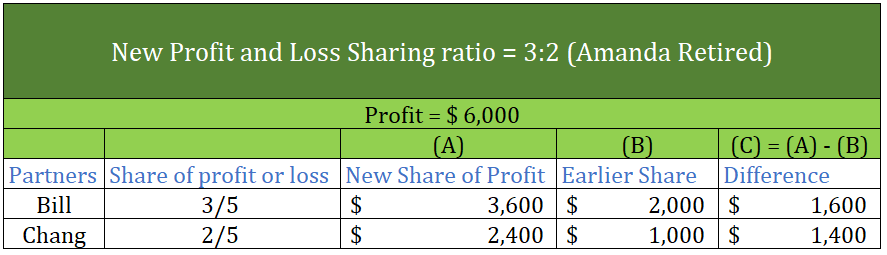

Suppose, upon retirement of Amanda, Bill and Chang change the P/L sharing between them to from 2:1 to 3:2

In that case,

- The gain ratio of Bill = 3/5 – 2/6 = 8/30

- The gain ratio of Chang = 2/5 – 1/6 = 7/30

Therefore the gain ratio in which Bill and Chang will gain the share of profit of Amanda is 8/30 : 7/30 or simply 8:7

To proceed with how to make a partnership deed, let me explain to you in short what is partnership deed? A partnership deed is the written agreement between the partners who have agreed to share profits of a business carried on by them. This basically contains terms and conditions to be followed betRead more

To proceed with how to make a partnership deed, let me explain to you in short what is partnership deed?

A partnership deed is the written agreement between the partners who have agreed to share profits of a business carried on by them. This basically contains terms and conditions to be followed between the partners.

Few contents of the partnership deed are as follows:

Generally, a partnership deed contains all those matters which can affect the relationship between the partners. However, if there is no such agreement the partnership should follow the provisions mentioned under The Partnership Act, 1932.

Now coming to the main question how to make a partnership deed? See the process is not so complicated. The partnership deed may be oral or written, but as the oral agreement has no value for obtaining tax benefits, a partnership firm always prefers a written agreement.

To prepare the same the partnership deed must be prepared on a stamp paper and signed by all the partners as per Indian Stamp Act and copies of the same should be with all the partners and also must be filed by the registrar of the firm.

A deed may vary depending on the nature of the partnership they are engaged in. Generally, partnerships are of three types

the process of making deed is same for all but, the content of deed may vary depending on the liability of partners in the partnership.

Further to know more about the registration process of partnership firm you can refer the following link https://www.mca.gov.in/Ministry/actsbills/pdf/Partnership_Act_1932.pdf

See less