The correct option is C. Either Debit or Credit. Partner’s Current account is prepared when the capital account is of fixed nature. We know that partner’s capital account can be of fluctuating nature or fixed nature. In the case of fluctuating partner’s capital, all the transactions relating to theRead more

The correct option is C. Either Debit or Credit.

Partner’s Current account is prepared when the capital account is of fixed nature. We know that partner’s capital account can be of fluctuating nature or fixed nature.

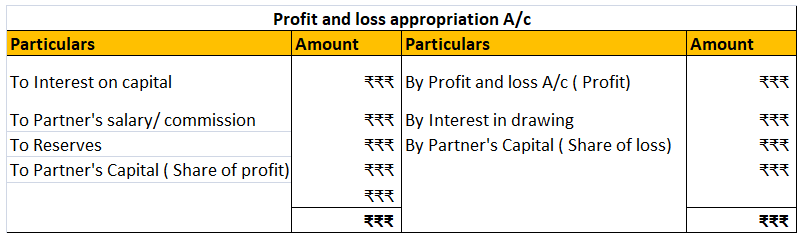

In the case of fluctuating partner’s capital, all the transactions relating to the appropriation of profit, salary, commission, drawings, the introduction of capital, interest on capital etc. are passed through the partner’s capital account.

The balance of partner’s capital is generally credit but sometimes it may show debit balance indicating that the business owes to partner.

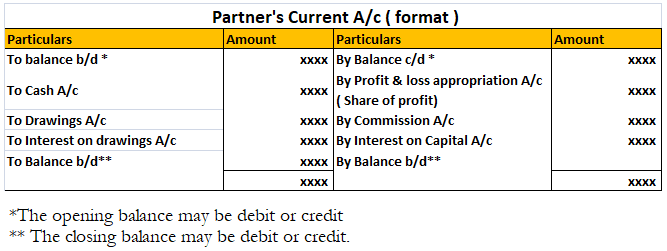

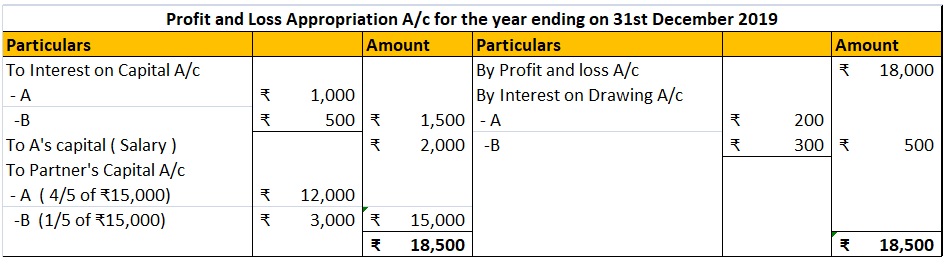

But when the partner’s capital account is of fixed nature, then separate partner’ current accounts are prepared. Through this account, all the transactions of revenue nature are passed like appropriation of profits, salary or commission paid to a partner, interest on capital and drawings. The balance of this account may be debit or credit.

The debit balance means the partner has withdrawn a lot of amount as drawings in anticipation of profits. The credit balance means the partner owes to the business.

The partner’s capital shows a fixed amount as capital and its balance is affected only when additional capital is introduced or capital is withdrawn. The balance of this account is always credit.

The partner current account is prepared when the firm wants to show the revenue transactions and capital transactions related to the partner ‘capital separately.

See less

Partnership Firm Persons who have entered into a partnership with one another to carry on a business are individually called “Partners“; collectively called a “Partnership Firm”; and the name under which their business is carried on is called the “Firm Name” In simple words, A partnership is an agreRead more

Partnership Firm

Persons who have entered into a partnership with one another to carry on a business are individually called “Partners“; collectively called a “Partnership Firm”; and the name under which their business is carried on is called the “Firm Name”

In simple words, A partnership is an agreement between two or more people who comes together to run a business on a partnership deed, which is called a Partnership firm. A Partnership Deed is a written agreement between partners who are willing to form a Partnership Firm. It is also called a Partnership Agreement.

It has no separate legal entity which cannot be separated from the members. It is merely a collective name given to the individuals composing it. This means, a partnership firm cannot hold property in its name, and neither it can sue nor be sued by others.

Contents of a Partnership Deed

A Partnership Deed shall mainly include the following contents:

Types of Partners

The following are the various types o partners

Types of Partnership Firms

There are four types of partnership which are as below.

Essential characteristics of a partnership firm

See less